Policy reactions to the Eurozone crisis

The Eurozone crisis is an ongoing financial crisis that has made it difficult or impossible for some countries in the euro area to repay or re-finance their government debt without the assistance of third parties.

The European sovereign debt crisis resulted from a combination of complex factors, including the globalization of finance; easy credit conditions during the 2002–2008 period that encouraged high-risk lending and borrowing practices; the 2007–2012 global financial crisis; international trade imbalances; real-estate bubbles that have since burst; the 2008–2012 global recession; fiscal policy choices related to government revenues and expenses; and approaches used by nations to bail out troubled banking industries and private bondholders, assuming private debt burdens or socializing losses. [1][2]

One narrative describing the causes of the crisis begins with the significant increase in savings available for investment during the 2000–2007 period when the global pool of fixed-income securities increased from approximately $36 trillion in 2000 to $70 trillion by 2007. This "Giant Pool of Money" increased as savings from high-growth developing nations entered global capital markets. Investors searching for higher yields than those offered by U.S. Treasury bonds sought alternatives globally.[3]

The temptation offered by such readily available savings overwhelmed the policy and regulatory control mechanisms in country after country, as lenders and borrowers put these savings to use, generating bubble after bubble across the globe. While these bubbles have burst, causing asset prices (e.g., housing and commercial property) to decline, the liabilities owed to global investors remain at full price, generating questions regarding the solvency of governments and their banking systems.[1]

How each European country involved in this crisis borrowed and invested the money varies. For example, Ireland's banks lent the money to property developers, generating a massive property bubble. When the bubble burst, Ireland's government and taxpayers assumed private debts. In Greece, the government increased its commitments to public workers in the form of extremely generous wage and pension benefits, with the former doubling in real terms over 10 years.[4] Iceland's banking system grew enormously, creating debts to global investors (external debts) several times GDP.[1][5]

The three crucial problems of the European economic governance emerged during the crisis are the asymmetry in the policy-making process for centralized policies and decentralized ones, ambiguities related to the coherent functioning of the euro area and the EU as well as of distribution of powers between national institutions and supranational ones, which implies the dilemma of legitimacy of the European economic governance and its rules.[6]

The interconnection in the global financial system means that if one nation defaults on its sovereign debt or enters into recession putting some of the external private debt at risk, the banking systems of creditor nations face losses. For example, in October 2011, Italian borrowers owed French banks $366 billion (net). Should Italy be unable to finance itself, the French banking system and economy could come under significant pressure, which in turn would affect France's creditors and so on. This is referred to as financial contagion.[7][8] Another factor contributing to interconnection is the concept of debt protection. Institutions entered into contracts called credit default swaps (CDS) that result in payment should default occur on a particular debt instrument (including government issued bonds). But, since multiple CDSs can be purchased on the same security, it is unclear what exposure each country's banking system now has to CDS.[9]

Greece hid its growing debt and deceived EU officials with the help of derivatives designed by major banks.[10][11][12][13][14][15] Although some financial institutions clearly profited from the growing Greek government debt in the short run,[10] there was a long lead-up to the crisis.

EU emergency measures

The table below provides an overview of the financial composition of all bailout programs being initiated for EU member states, since the Global Financial Crisis erupted in September 2008. EU member states outside the eurozone (marked with yellow in the table) have no access to the funds provided by EFSF/ESM, but can be covered with rescue loans from EU's Balance of Payments programme (BoP), IMF and bilateral loans (with an extra possible assistance from the Worldbank/EIB/EBRD if classified as a development country). Since October 2012, the ESM as a permanent new financial stability fund to cover any future potential bailout packages within the eurozone, has effectively replaced the now defunct GLF + EFSM + EFSF funds. Whenever pledged funds in a scheduled bailout program were not transferred in full, the table has noted this by writing "Y out of X".

| EU member | Time span | IMF[16][17] (billion €) |

World Bank[17] (billion €) |

EIB / EBRD (billion €) |

Bilateral[16] (billion €) |

BoP[17] (billion €) |

GLF[18] (billion €) |

EFSM[16] (billion €) |

EFSF[16] (billion €) |

ESM[16] (billion €) |

Bailout in total (billion €) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Cyprus I1 | Dec.2011-Dec.2012 | - | - | - | 2.5 | - | - | - | - | - | 2.51 |

| Cyprus II2 | May 2013-Mar.2016 | 1.0 | - | - | - | - | - | - | - | 9.0 | 10.02 |

| Greece I+II3 | May 2010-Jun.2015 | 32.1 out of 48.1 | - | - | - | - | 52.9 | - | 130.9 out of 144.6 | - | 215.9 out of 245.63 |

| Greece III4 | Aug.2015-Aug.2018 | (proportion of 86, to be decided Oct.2015) |

- | - | - | - | - | - | - | (up till 86) | 864 |

| Hungary5 | Nov.2008-Oct.2010 | 9.1 out of 12.5 | 1.0 | - | - | 5.5 out of 6.5 | - | - | - | - | 15.6 out of 20.05 |

| Ireland6 | Nov.2010-Dec.2013 | 22.5 | - | - | 4.8 | - | - | 22.5 | 18.4 | - | 68.26 |

| Latvia7 | Dec.2008-Dec.2011 | 1.1 out of 1.7 | 0.4 | 0.1 | 0.0 out of 2.2 | 2.9 out of 3.1 | - | - | - | - | 4.5 out of 7.57 |

| Portugal8 | May 2011-Jun 2014 | 26.5 out of 27.4 | - | - | - | - | - | 24.3 out of 25.6 | 26.0 | - | 76.8 out of 79.08 |

| Romania I9 | May 2009-Jun 2011 | 12.6 out of 13.6 | 1.0 | 1.0 | - | 5.0 | - | - | - | - | 19.6 out of 20.69 |

| Romania II10 | Mar 2011-Jun 2013 | 0.0 out of 3.6 | 1.15 | - | - | 0.0 out of 1.4 | - | - | - | - | 1.15 out of 6.1510 |

| Romania III11 | Oct 2013-Sep 2015 | 0.0 out of 2.0 | 2.5 | - | - | 0.0 out of 2.0 | - | - | - | - | 2.5 out of 6.511 |

| Spain12 | July 2012-Dec.2013 | - | - | - | - | - | - | - | - | 41.3 out of 100 | 41.3 out of 10012 |

| Total payment | Nov.2008-Aug.2018 | 104.9 | 6.05 | 1.1 | 7.3 | 13.4 | 52.9 | 46.8 | 175.3 | 136.3 | 544.05 |

| 1 Cyprus received in late December 2011 a €2.5bn bilateral emergency bailout loan from Russia, to cover its governmental budget deficits and a refinancing of maturing governmental debts until 31 December 2012.[19][20][21] Initially the bailout loan was supposed to be fully repaid in 2016, but as part of establishment of the later following second Cypriot bailout programme, Russia accepted a delayed repayment in eight biannual tranches throughout 2018-2021 - while also lowering its requested interest rate from 4.5% to 2.5%.[22] | |||||||||||

| 2 When it became evident Cyprus needed an additional bailout loan to cover the government's fiscal operations throughout 2013-2015, on top of additional funding needs for recapitalization of the Cypriot financial sector, negotiations for such an extra bailout package started with the Troika in June 2012.[23][24][25] In December 2012 a preliminary estimate indicated, that the needed overall bailout package should have a size of €17.5bn, comprising €10bn for bank recapitalisation and €6.0bn for refinancing maturing debt plus €1.5bn to cover budget deficits in 2013+2014+2015, which in total would have increased the Cypriot debt-to-GDP ratio to around 140%.[26] The final agreed package however only entailed a €10bn support package, financed partly by IMF (€1bn) and ESM (€9bn),[27] because it was possible to reach a fund saving agreement with the Cypriot authorities, featuring a direct closure of the most troubled Laiki Bank and a forced bail-in recapitalisation plan for Bank of Cyprus.[28][29] The final conditions for activation of the bailout package was outlined by the Troika's MoU agreement in April 2013, and include: 1) Recapitalisation of the entire financial sector while accepting a closure of the Laiki bank, 2) Implementation of the anti-money laundering framework in Cypriot financial institutions, 3) Fiscal consolidation to help bring down the Cypriot governmental budget deficit, 4) Structural reforms to restore competitiveness and macroeconomic imbalances, 5) Privatization programme. The Cypriot debt-to-GDP ratio is on this background now forecasted only to peak at 126% in 2015 and subsequently decline to 105% in 2020, and thus considered to remain within sustainable territory. The €10bn bailout comprise €4.1bn spend on debt liabilities (refinancing and amortization), 3.4bn to cover fiscal deficits, and €2.5bn for the bank recapitalization. These amounts will be paid to Cyprus through regular tranches from 13 May 2013 until 31 March 2016. According to the programme this will be sufficient, as Cyprus during the programme period in addition will: Receive €1.0bn extraordinary revenue from privatization of government assets, ensure an automatic roll-over of €1.0bn maturing Treasury Bills and €1.0bn of maturing bonds held by domestic creditors, bring down the funding need for bank recapitalization with €8.7bn - of which 0.4bn is reinjection of future profit earned by the Cyprus Central Bank (injected in advance at the short term by selling its gold reserve) and €8.3bn origin from the bail-in of creditors in Laiki bank and Bank of Cyprus.[30] The forced automatic rollover of maturing bonds held by domestic creditors were conducted in 2013, and equaled according to some credit rating agencies a "selective default" or "restrictive default", mainly because of the fact that the fixed yields of the new bonds did not reflect the market rates - while maturities at the same time automatically were extended.[22] | |||||||||||

| 3 Many sources list the first bailout was €110bn followed by the second on €130bn. When you deduct €2.7bn due to Ireland+Portugal+Slovakia opting out as creditors for the first bailout, and add the extra €8.2bn IMF has promised to pay Greece for the years in 2015-16 (through a programme extension implemented in December 2012), the total amount of bailout funds sums up to €245.6bn.[18][31] The first bailout resulted in a payout of €20.1bn from IMF and €52.9bn from GLF, during the course of May 2010 until December 2011,[18] and then it was technically replaced by a second bailout package for 2012-2016, which had a size of €172.6bn (€28bn from IMF and €144.6bn from EFSF), as it included the remaining committed amounts from the first bailout package.[32] All committed IMF amounts were made available to the Greek government for financing its continued operation of public budget deficits and to refinance maturing public debt held by private creditors and IMF. The payments from EFSF were earmarked to finance €35.6bn of PSI restructured government debt (as part of a deal where private investors in return accepted a nominal haircut, lower interest rates and longer maturities for their remaining principal), €48.2bn for bank recapitalization,[31] €11.3bn for a second PSI debt buy-back,[33] while the remaining €49.5bn were made available to cover continued operation of public budget deficits.[34] The combined programme was scheduled to expire in March 2016, after IMF had extended their programme period with extra loan tranches from January 2015 to March 2016 (as a mean to help Greece service the total sum of interests accruing during the lifespan of already issued IMF loans), while the Eurogroup at the same time opted to conduct their reimbursement and deferral of interests outside their bailout programme framework - with the EFSF programme still being planned to end in December 2014.[35] Due to the refusal by the Greek government to comply with the agreed conditional terms for receiving a continued flow of bailout transfers, both IMF and the Eurogroup opted to freeze their programmes since August 2014. To avoid a technical expiry, the Eurogroup postponed the expiry date for its frozen programme to 30 June 2015, paving the way within this new deadline for the possibility of transfer terms first to be renegotiated and then finally complied with to ensure completion of the programme.[35] As Greece withdrew unilaterally from the process of settling renegotiated terms and time extension for the completion of the programme, it expired uncompleted on 30 June 2015. Hereby, Greece lost the possibility to extract €13.7bn of remaining funds from the EFSF (€1.0bn unused PSI and Bond Interest facilities, €10.9bn unused bank recapitalization funds and a €1.8bn frozen tranche of macroeconomic support),[36][37] and also lost the remaining SDR 13.561bn of IMF funds[38] (being equal to €16.0bn as per the SDR exchange rate on 5 Jan 2012[39]), although those lost IMF funds might be recouped if Greece settles an agreement for a new third bailout programme with ESM - and passes the first review of such programme. | |||||||||||

| 4 A new third bailout programme worth €86bn in total, jointly covered by funds from IMF and ESM, will be disbursed in tranches from August 2015 until August 2018.[40] The programme was approved to be negotiated on 17 July 2015,[41] and approved in full detail by the publication of an ESM facility agreement on 19 August 2015.[42][43] IMF's transfer of the "remainder of its frozen I+II programme" and their new commitment also to contribute with a part of the funds for the third bailout, depends on a successful prior completion of the first review of the new third programme in October 2015.[44] Due to a matter of urgency, EFSM immediately conducted a temporary €7.16bn emergency transfer to Greece on 20 July 2015,[45][46] which was fully overtaken by ESM when the first tranche of the third program was conducted 20 August 2015.[43] Due to being temporary bridge financing and not part of an official bailout programme, the table do not display this special type of EFSM transfer. The loans of the program has an average maturity of 32.5 years and carry a variable interest rate (currently at 1%). The program has earmarked transfer of up till €25bn for bank recapitalization purposes (to be used to the extent deemed needed by the annual stress tests of the SSM), and also include establishment of a new privatization fund to conduct sale of Greek public assets - of which the first generated €25bn will be used for early repayment of the bailout loans earmarked for bank recapitalizations. Potential debt relief for Greece, in the form of longer grace and payment periods, will be considered by the European public creditors after the first review of the new programme, by October/November 2015.[43] | |||||||||||

| 5 Hungary recovered faster than expected, and thus did not receive the remaining €4.4bn bailout support scheduled for October 2009-October 2010.[17][47] IMF paid in total 7.6 out of 10.5 billion SDR,[48] equal to €9.1bn out of €12.5bn at current exchange rates.[49] | |||||||||||

| 6 In Ireland the National Treasury Management Agency also paid €17.5bn for the program on behalf of the Irish government, of which €10bn were injected by the National Pensions Reserve Fund and the remaining €7.5bn paid by "domestic cash resources",[50] which helped increase the program total to €85bn.[16] As this extra amount by technical terms is an internal bail-in, it has not been added to the bailout total. As of 31 March 2014 all committed funds had been transferred, with EFSF even paying €0.7bn more, so that the total amount of funds had been marginally increased from €67.5bn to €68.2bn.[51] | |||||||||||

| 7 Latvia recovered faster than expected, and thus did not receive the remaining €3.0bn bailout support originally scheduled for 2011.[52][53] | |||||||||||

| 8 Portugal completed its support programme as scheduled in June 2014, one month later than initially planned due to awaiting a verdict by its constitutional court, but without asking for establishment of any subsequent precautionary credit line facility.[54] By the end of the programme all committed amounts had been transferred, except for the last tranche of €2.6bn (1.7bn from EFSM and 0.9bn from IMF),[55] which the Portuguese government declined to receive.[56][57] The reason why the IMF transfers still mounted to slightly more than the initially committed €26bn, was due to its payment with SDR's instead of euro - and some favorable developments in the EUR-SDR exchange rate compared to the beginning of the programme.[58] In November 2014, Portugal received its last delayed €0.4bn tranche from EFSM (post programme),[59] hereby bringing its total drawn bailout amount up at €76.8bn out of €79.0bn. | |||||||||||

| 9 Romania recovered faster than expected, and thus did not receive the remaining €1.0bn bailout support originally scheduled for 2011.[60][61] | |||||||||||

| 10 Romania had a precautionary credit line with €5.0bn available to draw money from if needed, during the period March 2011-June 2013; but entirely avoided to draw on it.[62][63][17][64] During the period, the World Bank however supported with a transfer of €0.4bn as a DPL3 development loan programme and €0.75bn as results based financing for social assistance and health.[65] | |||||||||||

| 11 Romania had a second €4bn precautionary credit line established jointly by IMF and EU, of which IMF accounts for SDR 1.75134bn = €2bn, which is available to draw money from if needed during the period from October 2013 to 30 September 2015. In addition the World Bank also made €1bn available under a Development Policy Loan with a deferred drawdown option valid from January 2013 through December 2015.[66] The World Bank will throughout the period also continue providing earlier committed development programme support of €0.891bn,[67][68] but this extra transfer is not accounted for as "bailout support" in the third programme due to being "earlier committed amounts". In April 2014, the World Bank increased their support by adding the transfer of a first €0.75bn Fiscal Effectiveness and Growth Development Policy Loan,[69] with the final second FEG-DPL tranch on €0.75bn (worth about $1bn) to be contracted in the first part of 2015.[70] No money had been drawn from the precautionary credit line, as of May 2014. | |||||||||||

| 12 Spain's €100bn support package has been earmarked only for recapitalisation of the financial sector.[71] Initially an EFSF emergency account with €30bn was available, but nothing was drawn, and it was cancelled again in November 2012 after being superseded by the regular ESM recapitalisation programme.[72] The first ESM recapitalisation tranch of €39.47bn was approved 28 November,[73][74] and transferred to the bank recapitalisation fund of the Spanish government (FROB) on 11 December 2012.[72] A second tranch for "category 2" banks on €1.86n was approved by the Commission on 20 December,[75] and finally transferred by ESM on 5 February 2013.[76] "Category 3" banks were also subject for a possible third tranch in June 2013, in case they failed before then to acquire sufficient additional capital funding from private markets.[77] During January 2013, all "category 3" banks however managed to fully recapitalise through private markets and thus will not be in need for any State aid. The remaining €58.7bn of the initial support package is thus not expected to be activated, but will stay available as a fund with precautionary capital reserves to possibly draw upon if unexpected things happen - until 31 December 2013.[71][78] In total €41.3bn out of the available €100bn was transferred.[79] Upon the scheduled exit of the programme, no follow-up assistance was requested.[80] | |||||||||||

European Financial Stability Facility (EFSF)

On 9 May 2010, the 27 EU member states agreed to create the European Financial Stability Facility, a legal instrument[81] aiming at preserving financial stability in Europe by providing financial assistance to eurozone states in difficulty. The EFSF can issue bonds or other debt instruments on the market with the support of the German Debt Management Office to raise the funds needed to provide loans to eurozone countries in financial troubles, recapitalize banks or buy sovereign debt.[82]

Emissions of bonds are backed by guarantees given by the euro area member states in proportion to their share in the paid-up capital of the European Central Bank. The €440 billion lending capacity of the facility is jointly and severally guaranteed by the eurozone countries' governments and may be combined with loans up to €60 billion from the European Financial Stabilisation Mechanism (reliant on funds raised by the European Commission using the EU budget as collateral) and up to €250 billion from the International Monetary Fund (IMF) to obtain a financial safety net up to €750 billion.[83]

The EFSF issued €5 billion of five-year bonds in its inaugural benchmark issue 25 January 2011, attracting an order book of €44.5 billion. This amount is a record for any sovereign bond in Europe, and €24.5 billion more than the European Financial Stabilisation Mechanism (EFSM), a separate European Union funding vehicle, with a €5 billion issue in the first week of January 2011.[84]

On 29 November 2011, the member state finance ministers agreed to expand the EFSF by creating certificates that could guarantee up to 30% of new issues from troubled euro-area governments, and to create investment vehicles that would boost the EFSF’s firepower to intervene in primary and secondary bond markets.[85]

Reception by financial markets

Stocks surged worldwide after the EU announced the EFSF's creation. The facility eased fears that the Greek debt crisis would spread,[86] and this led to some stocks rising to the highest level in a year or more.[87] The euro made its biggest gain in 18 months,[88] before falling to a new four-year low a week later.[89] Shortly after the euro rose again as hedge funds and other short-term traders unwound short positions and carry trades in the currency.[90] Commodity prices also rose following the announcement.[91]

The dollar Libor held at a nine-month high.[92] Default swaps also fell.[93] The VIX closed down a record almost 30%, after a record weekly rise the preceding week that prompted the bailout.[94] The agreement is interpreted as allowing the ECB to start buying government debt from the secondary market which is expected to reduce bond yields.[95] As a result, Greek bond yields fell sharply from over 10% to just over 5%.[96] Asian bonds yields also fell with the EU bailout.[97])

Usage of EFSF funds

The EFSF only raises funds after an aid request is made by a country.[98] As of the end of July 2012, it has been activated various times. In November 2010, it financed €17.7 billion of the total €67.5 billion rescue package for Ireland (the rest was loaned from individual European countries, the European Commission and the IMF). In May 2011 it contributed one third of the €78 billion package for Portugal. As part of the second bailout for Greece, the loan was shifted to the EFSF, amounting to €164 billion (130bn new package plus 34.4bn remaining from Greek Loan Facility) throughout 2014.[99] On 20 July 2012, European finance ministers sanctioned the first tranche of a partial bail-out worth up to €100 billion for Spanish banks.[100] This leaves the EFSF with €148 billion[100] or an equivalent of €444 billion in leveraged firepower.[101]

The EFSF is set to expire in 2013, running some months parallel to the permanent €500 billion rescue funding program called the European Stability Mechanism (ESM), which will start operating as soon as member states representing 90% of the capital commitments have ratified it. (see section: ESM)

On 13 January 2012, Standard & Poor’s downgraded France and Austria from AAA rating, lowered Spain, Italy (and five other[102]) euro members further, and maintained the top credit rating for Finland, Germany, Luxembourg, and the Netherlands; shortly after, S&P also downgraded the EFSF from AAA to AA+.[102][103]

European Financial Stabilisation Mechanism (EFSM)

On 5 January 2011, the European Union created the European Financial Stabilisation Mechanism (EFSM), an emergency funding programme reliant upon funds raised on the financial markets and guaranteed by the European Commission using the budget of the European Union as collateral.[104] It runs under the supervision of the Commission[105] and aims at preserving financial stability in Europe by providing financial assistance to EU member states in economic difficulty.[106] The Commission fund, backed by all 27 European Union members, has the authority to raise up to €60 billion[107] and is rated AAA by Fitch, Moody's and Standard & Poor's.[108][109]

Under the EFSM, the EU successfully placed in the capital markets a €5 billion issue of bonds as part of the financial support package agreed for Ireland, at a borrowing cost for the EFSM of 2.59%.[110]

Like the EFSF, the EFSM was replaced by the permanent rescue funding programme ESM, which was launched in September 2012.[111]

Brussels agreement and aftermath

On 26 October 2011, leaders of the 17 eurozone countries met in Brussels and agreed on a 50% write-off of Greek sovereign debt held by banks, a fourfold increase (to about €1 trillion) in bail-out funds held under the European Financial Stability Facility, an increased mandatory level of 9% for bank capitalisation within the EU and a set of commitments from Italy to take measures to reduce its national debt. Also pledged was €35 billion in "credit enhancement" to mitigate losses likely to be suffered by European banks. José Manuel Barroso characterised the package as a set of "exceptional measures for exceptional times".[112][113]

The package's acceptance was put into doubt on 31 October when Greek Prime Minister George Papandreou announced that a referendum would be held so that the Greek people would have the final say on the bailout, upsetting financial markets.[114] On 3 November 2011 the promised Greek referendum on the bailout package was withdrawn by Prime Minister Papandreou.

In late 2011, Landon Thomas in the New York Times noted that some, at least, European banks were maintaining high dividend payout rates and none were getting capital injections from their governments even while being required to improve capital ratios. Thomas quoted Richard Koo, an economist based in Japan, an expert on that country's banking crisis, and specialist in balance sheet recessions, as saying:

I do not think Europeans understand the implications of a systemic banking crisis.... When all banks are forced to raise capital at the same time, the result is going to be even weaker banks and an even longer recession – if not depression.... Government intervention should be the first resort, not the last resort.

Beyond equity issuance and debt-to-equity conversion, then, one analyst "said that as banks find it more difficult to raise funds, they will move faster to cut down on loans and unload lagging assets" as they work to improve capital ratios. This latter contraction of balance sheets "could lead to a depression”, the analyst said.[115] Reduced lending was a circumstance already at the time being seen in a "deepen[ing] crisis" in commodities trade finance in western Europe.[116]

Final agreement on the second bailout package

In a marathon meeting on 20/21 February 2012 the Eurogroup agreed with the IMF and the Institute of International Finance on the final conditions of the second bailout package worth €130 billion. The lenders agreed to increase the nominal haircut from 50% to 53.5%. EU Member States agreed to an additional retroactive lowering of the interest rates of the Greek Loan Facility to a level of just 150 basis points above the Euribor. Furthermore, governments of Member States where central banks currently hold Greek government bonds in their investment portfolio commit to pass on to Greece an amount equal to any future income until 2020. Altogether this should bring down Greece's debt to between 117%[117] and 120.5% of GDP by 2020.[118]

European Central Bank

The European Central Bank (ECB) has taken a series of measures aimed at reducing volatility in the financial markets and at improving liquidity.[119]

In May 2010 it took the following actions:

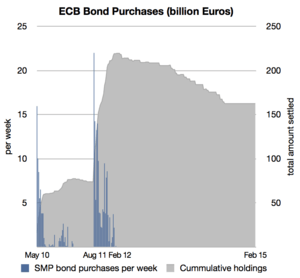

- It began open market operations buying government and private debt securities,[120] reaching €219.5 billion in February 2012,[121] though it simultaneously absorbed the same amount of liquidity to prevent a rise in inflation.[122] According to Rabobank economist Elwin de Groot, there is a “natural limit” of €300 billion the ECB can sterilize.[123]

- It reactivated the dollar swap lines[124] with Federal Reserve support.[125]

- It changed its policy regarding the necessary credit rating for loan deposits, accepting as collateral all outstanding and new debt instruments issued or guaranteed by the Greek government, regardless of the nation's credit rating.

The move took some pressure off Greek government bonds, which had just been downgraded to junk status, making it difficult for the government to raise money on capital markets.[126]

On 30 November 2011, the ECB, the U.S. Federal Reserve, the central banks of Canada, Japan, Britain and the Swiss National Bank provided global financial markets with additional liquidity to ward off the debt crisis and to support the real economy. The central banks agreed to lower the cost of dollar currency swaps by 50 basis points to come into effect on 5 December 2011. They also agreed to provide each other with abundant liquidity to make sure that commercial banks stay liquid in other currencies.[127]

Long Term Refinancing Operation (LTRO)

Though the ECB's main refinancing operations (MRO) are from repo auctions with a (bi)weekly maturity and monthly maturation, the ECB now conducts Long Term Refinancing Operations (LTROs), maturing after three months, six months, 12 months and 36 months. In 2003, refinancing via LTROs amounted to 45 bln euro which is about 20% of overall liquidity provided by the ECB.[128]

The ECB's first supplementary longer-term refinancing operation (LTRO) with a six-month maturity was announced March 2008.[129] Previously the longest tender offered was three months. It announced two 3-month and one 6-month full allotment of Long Term Refinancing Operations (LTROs). The first tender was settled 3 April, and was more than four times oversubscribed. The €25 billion auction drew bids amounting to €103.1 billion, from 177 banks. Another six-month tender was allotted on 9 July, again to the amount of €25 billion.[129] The first 12-month LTRO in June 2009 had close to 1100 bidders.[130]

On 22 December 2011, the ECB[131] started the biggest infusion of credit into the European banking system in the euro's 13-year history. Under its Long Term Refinancing Operations (LTROs) it loaned €489 billion to 523 banks for an exceptionally long period of three years at a rate of just one percent.[132] Previous refinancing operations matured after three, six and twelve months.[130] The by far biggest amount of €325 billion was tapped by banks in Greece, Ireland, Italy and Spain.[133]

This way the ECB tried to make sure that banks have enough cash to pay off €200 billion of their own maturing debts in the first three months of 2012, and at the same time keep operating and loaning to businesses so that a credit crunch does not choke off economic growth. It also hoped that banks would use some of the money to buy government bonds, effectively easing the debt crisis.[134] On 29 February 2012, the ECB held a second auction, LTRO2, providing 800 Eurozone banks with further €529.5 billion in cheap loans.[135] Net new borrowing under the €529.5 billion February auction was around €313 billion; out of a total of €256 billion existing ECB lending (MRO + 3m&6m LTROs), €215 billion was rolled into LTRO2.[136]

ECB lending has largely replaced inter-bank lending. Spain has €365 billion and Italy has €281 billion of borrowings from the ECB (June 2012 data). Germany has €275 billion on deposit.[137]

Resignations

In September 2011, Jürgen Stark became the second German after Axel A. Weber to resign from the ECB Governing Council in 2011. Weber, the former Deutsche Bundesbank president, was once thought to be a likely successor to Jean-Claude Trichet as bank president. He and Stark were both thought to have resigned due to "unhappiness with the ECB’s bond purchases, which critics say erode the bank’s independence". Stark was "probably the most hawkish" member of the council when he resigned. Weber was replaced by his Bundesbank successor Jens Weidmann, while Belgium's Peter Praet took Stark's original position, heading the ECB's economics department.[138]

Money supply growth

In April, 2012, statistics showed a growth trend in the M1 "core" money supply. Having fallen from an over 9% growth rate in mid-2008 to negative 1% +/- for several months in 2011, M1 core has built to a 2-3% range in early 2012. "'It is still early days but a further recovery in peripheral real M1 would suggest an end to recessions by late 2012,' said Simon Ward from Henderson Global Investors who collects the data." While attributing the money supply growth to ECB's LTRO policies, an analysis in The Telegraph said lending "continued to fall across the eurozone in March [and] ... [t]he jury is out on the ... three-year lending adventure (LTRO)".[139]

Reorganization of the European banking system

On June 16, 2012, the European Central Bank together with other European leaders hammered out plans for the ECB to become a bank regulator and to form a deposit insurance program to augment national programs. Other economic reforms promoting European growth and employment were also proposed.[140]

Outright Monetary Transactions (OMTs)

On 6 September 2012, the ECB announced to offer additional financial support in the form of some yield-lowering bond purchases (OMT), for all eurozone countries involved in a sovereign state bailout program from EFSF/ESM.[141] A eurozone country can benefit from the program if – and for as long as – it is found to suffer from stressed bond yields at excessive levels; but only at the point of time where the country possesses/regains a complete market access – and only if the country still comply with all terms in the signed Memorandum of Understanding (MoU) agreement.[141][142] Countries receiving a precautionary programme rather than a sovereign bailout, will per definition have complete market access and thus qualify for OMT support if also suffering from stressed interest rates on its government bonds. In regards of countries receiving a sovereign bailout (Ireland, Portugal and Greece), they will on the other hand not qualify for OMT support before they have regained complete market access, which will normally only happen after having received the last scheduled bailout disbursement.[141][143] Despite none OMT programmes were ready to start in September/October, the financial markets straight away took notice of the additionally planned OMT packages from ECB, and started slowly to price-in a decline of both short-term and long-term interest rates in all European countries previously suffering from stressed and elevated interest levels (as OMTs were regarded as an extra potential back-stop to counter the frozen liquidity and highly stressed rates; and just the knowledge about their potential existence in the very near future helped to calm the markets).

If Spain signs a negotiated Memorandum of Understanding with the Troika (EC, ECB and IMF) outlining ESM shall offer a precautionary programme with credit lines for the Spanish government to potentially draw on if needed (beside of the bank recapitalisation package they already applied for), this would qualify Spain also to receive the OMT support from ECB, as the sovereign state would still continue to operate with a complete market access with the precautionary conditioned credit line. In regards of Ireland, Portugal and Greece, they on the other hand have not yet regained complete market access, and thus do not yet qualify for OMT support.[141][143]

European Stability Mechanism (ESM)

The European Stability Mechanism (ESM) is a permanent rescue funding programme to succeed the temporary European Financial Stability Facility and European Financial Stabilisation Mechanism in July 2012[111] but it had to be postponed until after the Federal Constitutional Court of Germany had confirmed the legality of the measures on 12 September 2012.[144][145] The permanent bailout fund entered into force for 16 signatories on 27 September 2012. It became effective in Estonia on 4 October 2012 after the completion of their ratification process.[146]

On 16 December 2010 the European Council agreed a two line amendment to the EU Lisbon Treaty to allow for a permanent bail-out mechanism to be established[147] including stronger sanctions. In March 2011, the European Parliament approved the treaty amendment after receiving assurances that the European Commission, rather than EU states, would play 'a central role' in running the ESM.[148][149] The ESM is an intergovernmental organisation under public international law. It is located in Luxembourg.[150][151]

Such a mechanism serves as a "financial firewall." Instead of a default by one country rippling through the entire interconnected financial system, the firewall mechanism can ensure that downstream nations and banking systems are protected by guaranteeing some or all of their obligations. Then the single default can be managed while limiting financial contagion.

European Fiscal Compact

In March 2011 a new reform of the Stability and Growth Pact was initiated, aiming at straightening the rules by adopting an automatic procedure for imposing of penalties in case of breaches of either the 3% deficit or the 60% debt rules.[152][153] By the end of the year, Germany, France and some other smaller EU countries went a step further and vowed to create a fiscal union across the eurozone with strict and enforceable fiscal rules and automatic penalties embedded in the EU treaties.[154][155] On 9 December 2011 at the European Council meeting, all 17 members of the eurozone and six countries that aspire to join agreed on a new intergovernmental treaty to put strict caps on government spending and borrowing, with penalties for those countries who violate the limits.[156] All other non-eurozone countries apart from the UK are also prepared to join in, subject to parliamentary vote.[111] The treaty will enter into force on 1 January 2013, if by that time 12 members of the euro area have ratified it.[157]

Originally EU leaders planned to change existing EU treaties but this was blocked by British prime minister David Cameron, who demanded that the City of London be excluded from future financial regulations, including the proposed EU financial transaction tax.[158][159] By the end of the day, 26 countries had agreed to the plan, leaving the United Kingdom as the only country not willing to join.[160] Cameron subsequently conceded that his action had failed to secure any safeguards for the UK.[161] Britain's refusal to be part of the fiscal compact to safeguard the eurozone constituted a de facto refusal (PM David Cameron vetoed the project) to engage in any radical revision of the Lisbon Treaty. John Rentoul of The Independent concluded that "Any Prime Minister would have done as Cameron did".[162]

See also

- 2000s commodities boom

- 2007–2012 global financial crisis

- 2008–2012 Icelandic financial crisis

- 2008–2012 global recession

- Crisis situations and protests in Europe since 2000

- European sovereign-debt crisis: List of acronyms

- European sovereign-debt crisis: List of protagonists

- Federal Reserve Economic Data FRED

- Late-2000s recession in Europe

- List of countries by credit rating

- DiEM 2025 (Democracy in Europe Movement⋅2025)

References

- 1 2 3 Lewis, Michael (2011). Boomerang: Travels in the New Third World. Norton. ISBN 978-0-393-08181-7.]

- ↑ Lewis, Michael (2011-09-26). "Touring the Ruins of the Old Economy". New York Times. Retrieved 2012-06-06.

- ↑ "NPR-The Giant Pool of Money-May 2008". Thisamericanlife.org. Retrieved 2012-05-14.

- ↑ Heard on Fresh Air from WHYY (2011-10-04). "NPR-Michael Lewis-How the Financial Crisis Created a New Third World-October 2011". Npr.org. Retrieved 2012-07-07.

- ↑ LEWIS Michael (April 2009). "Wall Street on the Tundra". Vanity Fair. VanityFair.com. Retrieved 2012-07-18.

In the end, Icelanders amassed debts amounting to 850 percent of their G.D.P. (The debt-drowned United States has reached just 350 percent.)

- ↑ Laruffa Matteo, The European Economic Governance: Problems and Proposals for Institutional Innovations, Winning Paper for the Annual Meeting Progressive Economy, Brussels, 6 March 2014.

- ↑ Seth W. Feaster; Nelson D. Schwartz; Tom Kuntz (2011-10-22). "NYT-It's All Connected-A Spectators Guide to the Euro Crisis". New York Times. New York: Nytimes.com. Retrieved 2012-05-14.

- ↑ XAQUÍN G.V.; Alan McLEAN; Archie TSE (2011-10-22). "NYT-It's All Connected-An Overview of the Euro Crisis-October 2011". New York Times. Europe; Germany; Greece; France; Ireland; Spain; Portugal; Italy; Great Britain; United States; Japan: Nytimes.com. Retrieved 2012-05-14.

- ↑ Sponsored by (29 October 2011). "The Economist-No Big Bazooka-29 October 2011". Economist.com. Retrieved 2012-05-14.

- 1 2 Story, Louise; Landon Thomas Jr.; Nelson D. Schwartz (14 February 2010). "Wall St. Helped to Mask Debt Fueling Europe's Crisis". New York Times. New York. pp. A1. Retrieved 19 September 2011.

- ↑ "Merkel Slams Euro Speculation, Warns of 'Resentment' (Update 1)". BusinessWeek. 23 February 2010. Retrieved 28 April 2010.

- ↑ Laurence Knight (22 December 2010). "Europe's Eastern Periphery". BBC. Retrieved 17 May 2011.

- ↑ "PIIGS Definition". investopedia.com. Retrieved 17 May 2011.

- ↑ Bernd Riegert. "Europe's next bankruptcy candidates?". dw-world.com. Retrieved 17 May 2011.

- ↑ Nikolaos D. Philippas. Ζωώδη Ένστικτα και Οικονομικές Καταστροφές (in Greek). skai.gr. Retrieved 17 May 2011.

- 1 2 3 4 5 6 "FAQ about European Financial Stability Facility (EFSF) and the new ESM" (PDF). EFSF. 3 August 2012. Retrieved 19 August 2012.

- 1 2 3 4 5 "Balance of Payments - European Commission". Ec.europa.eu. 2013-01-31. Retrieved 2013-09-27.

- 1 2 3 http://ec.europa.eu/economy_finance/assistance_eu_ms/greek_loan_facility/index_en.htm

- ↑ "Cyprus Gets Second 1.32 Bln Euro Russian Loan Tranche". RiaNovosti. 26 January 2012. Retrieved 24 April 2013.

- ↑ "Russia loans Cyprus 2.5 billion". The Guardian. 10 October 2011. Archived from the original on 21 July 2012. Retrieved 13 March 2012.

- ↑ Hadjipapas, Andreas; Hope, Kerin (14 September 2011). "Cyprus nears €2.5bn Russian loan deal". Financial Times. Retrieved 13 March 2012.

- 1 2 "Public Debt Management Annual Report 2013" (PDF). Cypriot Ministry of Finance. 22 May 2014.

- ↑ "Eurogroup statement on a possible macro-financial assistance programme for Cyprus" (PDF). Eurogroup. 13 December 2012. Retrieved 14 December 2012.

- ↑ "European Commission statement on Cyprus". European Commission. 20 March 2013. Retrieved 24 March 2013.

- ↑ "Speech: Statement on Cyprus in the European Parliament (SPEECH/13/325 by Olli Rehn)". European Commission. 17 April 2013. Retrieved 23 April 2013.

- ↑ "Cyprus could lower debt post-bailout with ESM". Kathimerini (English edition). 12 December 2012. Retrieved 13 December 2012.

- ↑ "Eurogroup Statement on Cyprus" (PDF). Eurogroup. 12 April 2013. Retrieved 20 April 2013.

- ↑ "Eurogroup Statement on Cyprus". Eurozone Portal. 16 March 2013. Retrieved 24 March 2013.

- ↑ "Eurogroup Statement on Cyprus" (PDF). Eurogroup. 25 March 2013. Retrieved 25 March 2013.

- ↑ "The Economic Adjustment Programme for Cyprus" (PDF). Occasional Papers 149 (yield spreads displayed by graph 19). European Commission. 17 May 2013. Retrieved 19 May 2013.

- 1 2 "The Second Economic Adjustment Programme for Greece" (PDF). European Commission. March 2012. Retrieved 3 August 2012.

- ↑ "EFSF Head: Fund to contribute 109.1b euros to Greece's second bailout". Marketall. 16 March 2012.

- ↑ "FAQ – New disbursement of financial assistance to Greece" (PDF). EFSF. 22 January 2013.

- ↑ "The Second Economic Adjustment Programme for Greece (Third review July 2013)" (PDF). European Commission. 29 July 2013. Retrieved 22 January 2014.

- 1 2 "Frequently Asked Questions on the EFSF: Section E – The programme for Greece" (PDF). European Financial Stability Facility. 19 March 2015.

- ↑ "EFSF programme for Greece expires today". ESM. 30 June 2015.

- ↑ "FAQ document on Greece" (PDF). ESM. 13 July 2015.

- ↑ "Greece: Financial Position in the Fund as of June 30, 2015". IMF. 18 July 2015.

- ↑ "FIFTH REVIEW UNDER THE EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY, AND REQUEST FOR WAIVER OF NONOBSERVANCE OF PERFORMANCE CRITERION AND REPHASING OF ACCESS; STAFF REPORT; PRESS RELEASE; AND STATEMENT BY THE EXECUTIVE DIRECTOR FOR GREECE" (PDF). Table 13. Greece: Schedule of Proposed Purchases under the Extended Arrangement, 2012–16. IMF. 10 June 2014.

- ↑ "Greece: An Update of IMF Staff's Preliminary Public Debt Sustainability Analysis". IMF. 14 July 2015.

- ↑ "ESM Board of Governors approves decision to grant, in principle, stability support to Greece". ESM. 17 July 2015.

- ↑ "Eurogroup statement on the ESM programme for Greece". Council of the European Union. 14 August 2015.

- 1 2 3 "FAQ on ESM/EFSF financial assistance for Greece" (PDF). ESM. 19 August 2015.

- ↑ "Angela Merkel sees IMF joining Greek bailout, floats debt relief". National Post (Financial Post). 17 August 2015.

- ↑ "Council implementing decision (EU) 2015/1181 of 17 July 2015: on granting short-term Union financial assistance to Greece". Official Journal of the EU. 18 July 2015.

- ↑ "EFSM: Council approves €7bn bridge loan to Greece". Council of the EU. 17 July 2015.

- ↑ "Third supplemental memorandum of understanding" (PDF). Retrieved 2013-09-27.

- ↑ "IMF Financial Activities - Update September 30, 2010". Imf.org. Retrieved 2013-09-27.

- ↑ "Convert Euros (EUR) and Special Drawing Rights (SDR): Currency Exchange Rate Conversion Calculator". Coinmill.com. Retrieved 2013-09-27.

- ↑ "Dáil Éireann Debate (Vol.733 No.1): Written Answers - National Cash Reserves". Houses of the Oireachtas. 24 May 2011. Retrieved 26 April 2013.

- ↑ "Ireland's EU/IMF Programme: Programme Summary". National Treasury Management Agency. 31 March 2014.

- ↑ "Balance-of-payments assistance to Latvia". European Commission. 17 May 2013.

- ↑ "International Loan Programme: Questions and Answers". Latvian Finance Ministry.

- ↑ "Statement by Vice-President Siim Kallas on Portugal's decision regarding programme exit". European Commission. 5 May 2014.

- ↑ "Statement by the EC, ECB, and IMF on the Twelfth Review Mission to Portugal". IMF. 2 May 2014.

- ↑ "Portugal to do without final bailout payment". EurActiv. 13 June 2014.

- ↑ "The Economic Adjustment Programme for Portugal 2011-2014" (PDF). European Commission. 17 October 2014.

- ↑ "Occasional Papers 191: The Economic Adjustment Programme for Portugal Eleventh Review" (PDF). ANNEX 3: Indicative Financing Needs and Sources. European Commission. 23 April 2014.

- ↑ "Portugal: Final disbursement made from EU financial assistance programme". European Commission. 12 November 2014.

- ↑ "IMF Financial Activities - Update March 24, 2011". Imf.org. Retrieved 2013-09-27.

- ↑ "Convert Euros (EUR) and Special Drawing Rights (SDR): Currency Exchange Rate Conversion Calculator". Coinmill.com. Retrieved 2013-09-27.

- ↑ "IMF Financial Activities - Update September 27, 2012". Imf.org. Retrieved 2013-09-27.

- ↑ "Convert Euros (EUR) and Special Drawing Rights (SDR): Currency Exchange Rate Conversion Calculator". Coinmill.com. Retrieved 2013-09-27.

- ↑ "Press release: IMF Approves Three-Month Extension of SBA for Romania". IMF. 20 March 2013. Retrieved 26 April 2013.

- ↑ "Occasional Papers 156: Overall assessment of the two balance-of-payments assistance programmes for Romania, 2009-2013" (PDF). ANNEX 1: Financial Assistance Programmes in 2009-2013. European Commission. July 2013.

- ↑ "2013/531/EU: Council Decision of 22 October 2013 providing precautionary Union medium-term financial assistance to Romania" (PDF). Official Journal of the European Union. 29 October 2013.

- ↑ "WORLD BANK GROUP Romania Partnership: COUNTRY PROGRAM SNAPSHOT" (PDF). World Bank. April 2014.

- ↑ "Occasional Papers 165 - Romania: Balance-of-Payments Assistance Programme 2013-2015" (PDF). ANNEX 1: Financial Assistance Programmes in 2009-2013. European Commission. November 2013.

- ↑ "PROGRAM DOCUMENT ON A PROPOSED LOAN IN THE AMOUNT OF €750 MILLION TO ROMANIA: FOR THE FIRST FISCAL EFFECTIVENESS AND GROWTH DEVELOPMENT POLICY LOAN" (PDF). World Bank - IBRD. 29 April 2014.

- ↑ "World Bank launched Romania's Country Partnership Strategy for 2014-2017" (PDF). ACTMedia - Romanian Business News. 29 May 2014.

- 1 2 "Financial Assistance Facility Agreement between ESM, Spain, Bank of Spain and FROB" (PDF). European Commission. 29 November 2012. Retrieved 8 December 2012.

- 1 2 "FAQ - Financial Assistance for Spain" (PDF). ESM. 7 December 2012. Retrieved 8 December 2012.

- ↑ "State aid: Commission approves restructuring plans of Spanish banks BFA/Bankia, NCG Banco, Catalunya Banc and Banco de Valencia". Europa (European Commission). 28 November 2012. Retrieved 3 December 2012.

- ↑ "Spain requests €39.5bn bank bail-out, but no state rescue". The Telegraph. 3 December 2012. Retrieved 3 December 2012.

- ↑ "State aid: Commission approves restructuring plans of Spanish banks Liberbank, Caja3, Banco Mare Nostrum and Banco CEISS". Europa (European Commission). 20 December 2012. Retrieved 29 December 2012.

- ↑ "ESM financial assistance to Spain". ESM. 5 February 2013. Retrieved 5 February 2013.

- ↑ "European Economy Occasional Papers 118: The Financial Sector Adjustment Programme for Spain" (PDF). European Commission. 16 October 2012. Retrieved 28 October 2012.

- ↑ "European Economy Occasional Papers 130: Financial Assistance Programme for the Recapitalisation of Financial Institutions in Spain - Second Review of the Programme Spring 2013". European Commission. 19 March 2013. Retrieved 24 March 2013.

- ↑ "Spain's exit". ESM. 31 December 2013.

- ↑ "Spain successfully exits ESM financial assistance programme". ESM. 31 December 2013.

- ↑ The EFSF, "a legal instrument agreed by finance ministers earlier this month following the risk of Greece's debt crisis spreading to other weak economies."

- ↑ Thesing, Gabi (2011-01-22). "European Rescue Fund May Buy Bonds, Recapitalize Banks, ECB's Stark Says". Bloomberg. Retrieved 2012-05-16.

- ↑ Europeanvoice.com "Media reports said that Spain would ask for support from two EU funds for eurozone governments in financial difficulty: a €60bn ‘European financial stabilisation mechanism', which is reliant on guarantees from the EU budget."

- ↑ "Euromoney – International banking finance and capital markets news and analysis". Euromoney.com. Retrieved 2012-05-16.

- ↑ "TEXT-Euro zone finance ministers approve extending EFSF capacity". Reuters. UK. 29 November 2011. Retrieved 10 May 2010.

- ↑ "European Markets Surge". The Wall Street Journal. 10 May 2010. Retrieved 24 February 2012.

- ↑ Silberstein, Daniela (10 May 2010). "European Shares Jump Most in 17 Months as EU Pledges Loan Fund". Bloomberg. Retrieved 15 April 2011.

- ↑ Traynor, Ian (10 May 2010). "Euro strikes back with biggest gamble in its 11-year history". The Guardian. UK. Retrieved 10 May 2010.

- ↑ Wearden, Graeme; Kollewe, Julia (17 May 2010). "Euro hits four-year low on fears debt crisis will spread". The Guardian. UK.

- ↑ Kitano, Masayuki (21 May 2010). "Euro surges in short-covering rally, Aussie soars". Reuters. Retrieved 21 May 2010.

- ↑ Chanjaroen, Chanyaporn (10 May 2010). "Oil, Copper, Nickel Jump on European Bailout Plan; Gold Drops". Bloomberg. Retrieved 15 April 2011.

- ↑ Jenkins, Keith (10 May 2010). "Dollar Libor Holds Near Nine-Month High After EU Aid". Bloomberg. Retrieved 15 April 2011.

- ↑ Moses, Abigail (10 May 2010). "Default Swaps Tumble After EU Goes 'All In': Credit Markets". Bloomberg. Retrieved 15 April 2011.

- ↑ Kearns, Jeff (10 May 2010). "VIX Plunges by Record 36% as Stocks Soar on European Loan Plan". Bloomberg. Retrieved 15 April 2011.

- ↑ "Shares and oil prices surge after EU loan deal". BBC. 10 May 2010. Retrieved 10 May 2010.

- ↑ Nazareth, Rita (10 May 2010). "Stocks, Commodities, Greek Bonds Rally on European Loan Package". Bloomberg. Retrieved 15 April 2011.

- ↑ McDonald, Sarah (10 May 2010). "Asian Bond Risk Tumbles Most in 18 Months on EU Loan Package". Bloomberg. Retrieved 15 April 2011.

- ↑ Stearns, Jonathan. "Euro-Area Ministers Seal Rescue-Fund Deal to Stem Debt Crisis". Bloomberg.com. Retrieved 2012-05-16.

- ↑ "European Financial Stability Facility (EFSF)" (PDF). European Commission. 15 March 2012. Retrieved 16 March 2012.

- 1 2 "The Spanish patient". Economist. 28 July 2012. Retrieved 3 August 2012.

- ↑ "Welches Land gehört zu den großen Sorgenkindern?". Sueddeutsche. 2 December 2011. Retrieved 3 December 2011.

- 1 2 Gibson, Kate, "S&P takes Europe's rescue fund down a notch", MarketWatch, 16 January 2012 2:37 pm EST. Retrieved 16 January 2012.

- ↑ Standard & Poor's Ratings Services quoted at "S&P cuts EFSF bail-out fund rating: statement in full". BBC. 16 January 2012.

Standard & Poor's Ratings Services today lowered the 'AAA' long-term issuer credit rating on the European Financial Stability Facility (EFSF) to 'AA+' from 'AAA'.... We lowered to 'AA+' the long-term ratings on two of the EFSF's previously 'AAA' rated guarantor members, France and Austria. The outlook on the long-term ratings on France and Austria is negative, indicating that we believe that there is at least a one-in-three chance that we will lower the ratings again in 2012 or 2013. We affirmed the ratings on the other 'AAA' rated EFSF members: Finland, Germany, Luxembourg, and The Netherlands.

- ↑ "EU bonds for Ireland bailout well-received on market". Xinhua. 6 January 2011. Retrieved 26 April 2011.

- ↑ "AFP: First EU bond for Ireland attracts strong demand: HSBC". Google. AFP. 5 January 2011. Retrieved 26 April 2011.

- ↑ Bartha, Emese (5 January 2011). "A Mixed Day for European Debt". The Wall Street Journal. Retrieved 26 April 2011.

- ↑ Jolly, David (5 January 2011). "Irish Bailout Begins as Europe Sells Billions in Bonds". The New York Times.

- ↑ https://web.archive.org/web/20121119081912/http://www.nasdaq.com/aspx/stock-market-news-story.aspx?storyid=201101050332dowjonesdjonline000213&title=eu-sets-price-guidance-on-five-year-euro-bond-at-swaps-+012-015. Archived from the original on 19 November 2012. Retrieved 1 February 2013. Missing or empty

|title=(help) - ↑ Robinson, Frances (21 December 2010). "EU's Bailout Bond Three Times Oversubscribed". The Wall Street Journal. Retrieved 26 April 2011.

- ↑ "il bond è stato piazzato al tasso del 2,59%". Movisol.org. Retrieved 26 April 2011.

- 1 2 3 "European Council Press releases". European Council. 9 December 2011. Retrieved 9 December 2011.

- ↑ "Leaders agree eurozone debt deal after late-night talks". BBC News. 27 October 2011. Retrieved 27 October 2011.

- ↑ Bhatti, Jabeen (27 October 2011). "EU leaders reach a deal to tackle debt crisis". USA Today. Retrieved 27 October 2011.

- ↑ "Greece debt crisis: Markets dive on Greek referendum". Bbc.co.uk. 2011-11-01. Retrieved 2012-05-16.

- ↑ Thomas, Landon, Jr., "Banks Retrench in Europe While Keeping Up Appearances" (limited no-charge access), The New York Times, 22 December 2011. Retrieved 2011-12-22.

- ↑ Blas, Javier, "Commodities trade finance crisis deepens" (limited no-charge access), Financial Times, 16 December 2011. Retrieved 21 December 2011.

- ↑ "Griechenland spart sich auf Schwellenland-Niveau herunter". Sueddeutsche. 13 March 2012. Retrieved 13 March 2012.

- ↑ "Eurogroup statement" (PDF). Eurogroup. 21 February 2012. Retrieved 21 February 2012.

- ↑ "ECB decides on measures to address severe tensions in financial markets". ECB. 10 May 2010. Retrieved 21 May 2010.

- ↑ "Bundesbank: "EZB darf nicht Staatsfinanzierer werden"". Die Presse. 3 January 2012. Retrieved 3 January 2012.

- ↑ "Summary of ad hoc communication". ECB. 13 February 2012. Retrieved 13 February 2012.

- ↑ "Summary of ad hoc communication: Related to monetary policy implementation issued by the ECB since 1 January 2007". ECB. 28 November 2011. Retrieved 1 December 2011.

- ↑ "ECB May Hit Bond Sterilization Limit in January, Rabobank Says". Bloomberg Businessweek. 8 September 2011. Retrieved 1 December 2011.

- ↑ "ECB: ECB decides on measures to address severe tensions in financial markets". Retrieved 10 May 2010.

- ↑ Lanman, Scott (10 May 2010). "Fed Restarts Currency Swaps as EU Debt Crisis Flares". Bloomberg. Retrieved 15 April 2011.

- ↑ Today11:17 a.m. 5 May 2010 (5 March 2010). "ECB suspends rating threshold for Greece debt". MarketWatch. Retrieved 5 May 2010.

- ↑ "Grosse Notenbanken versorgen Banken mit Liquidität – Kursfeuerwerk an den Börsen – auch SNB beteiligt". NZZ Online. 2010-11-23. Retrieved 2012-05-14.

- ↑ "THE LONGER TERM REFINANCING OPERATIONS OF THE ECB" (PDF). May 2004.

- 1 2 "ECB offers longer-term finance via six-month LTROs". May 2008.

- 1 2 "Markets live transcript 29 February 2012". February 2012.

- ↑ "ECB announces measures to support bank lending and money market activity". December 2011.

- ↑ "ECB Lends 489 Billion Euros for 3 Years, Exceeding Forecast". Business Week. 21 December 2011. Retrieved 27 January 2012.

- ↑ Wearden, Graeme; Fletcher, Nick (29 February 2012). "Eurozone crisis live: ECB to launch massive cash injection". The Guardian. London. Retrieved 29 February 2012.

- ↑ Ewing, Jack; Jolly, David (21 December 2011). "Banks in the euro zone must raise more than 200 billion euros in the first three months of 2012". New York Times. Retrieved 21 December 2011.

- ↑ Wearden, Graeme; Fletcher, Nick (29 February 2012). "Eurozone crisis live: ECB to launch massive cash injection". The Guardian. London. Retrieved 29 February 2012.

- ↑ "€529 billion LTRO 2 tapped by record 800 banks". Euromoney. 29 February 2012. Retrieved 29 February 2012.

- ↑ Charles Forelle and David Enrich (13 Jul 2012). "Euro-Zone Banks Cut Back Lending". Wall Street Journal.

- ↑ "Belgium's Praet to serve as ECB's chief economist". MarketWatch. 3 January 2012. Retrieved 12 February 2012.

- ↑ Evans-Pritchard, Ambrose, "A glimmer of hope for the austerity wasteland of South Europe?", The Telegraph economics blog, April 30, 2012. Growth rates read off "Euroland Real M1 Deposits (%6M)" chart in blog; source: Thomson Reuters Datastream. Retrieved 2012-05-01.

- ↑ Jack Ewing (June 16, 2012). "European Leaders to Present Plan to Quell the Crisis Quickly". The New York Times. Retrieved June 16, 2012.

- 1 2 3 4 "Technical features of Outright Monetary Transactions", ECB Press Release, 6 September 2012

- ↑ Stephen Castle and Melissa Eddy (7 Sep 2012). "Bond Plan Lowers Debt Costs, but Germany Grumbles". New York Times.

- 1 2 "Press conference (4 October 2012): Introductory statement to the press conference (with Q&A)". ECB. 4 October 2012. Retrieved 10 October 2012.

- ↑ "Court to Rule on Euro Measures on Sept. 12". Spiegel Online. 16 July 2012. Retrieved 3 August 2012.

- ↑ Peel, Quentin (12 September 2012). "German court backs ESM bailout fund". Financial Times. Retrieved 12 September 2012.

- ↑ Kaiser, Stefan; Rickens, Christian (2012-09-20). "Euro Zone Changing ESM to Satisfy German Court". Spiegel Online. Retrieved 2012-09-27.

- ↑ EUROPEAN COUNCIL 16–17 December 2010 CONCLUSIONS, European Council 17 December 2010

- ↑ Parliament approves Treaty change to allow stability mechanism, European Parliament

- ↑ "Retrieved 22 March 2011 Published 22 March 2011". Monstersandcritics.com. 2011-03-23. Retrieved 2012-05-14.

- ↑ "EUROPEAN COUNCIL 24/25 March 2011 CONCLUSIONS" (PDF). Retrieved 2012-05-14.

- ↑ TREATY ESTABLISHING THE EUROPEAN STABILITY MECHANISM (ESM) between Belgium, Germany, Estonia, Ireland, Greece, Spain, France, Italy, Cyprus, Luxembourg, Malta, Netherlands, Austria, Portugal, Slovenia, Slovakia, and Finland; Council of the European Union.

- ↑ "Council reaches agreement on measures to strengthen economic governance" (PDF). Retrieved 15 April 2011.

- ↑ Jan Strupczewski (15 March 2011). "EU finmins adopt tougher rules against debt, imbalance". Uk.finance.yahoo.com. Retrieved 15 April 2011.

- ↑ Pidd, Helen (2 December 2011). "Angela Merkel vows to create 'fiscal union' across eurozone". The Guardian. London. Retrieved 2 December 2011.

- ↑ "European fiscal union: what the experts say". The Guardian. London. 2 December 2011. Retrieved 2 December 2011.

- ↑ Baker, Luke (9 December 2011). "WRAPUP 5-Europe moves ahead with fiscal union, UK isolated". Reuters. Retrieved 9 December 2011.

- ↑ "The fiscal compact ready to be signed". European Commission. 31 January 2012. Retrieved 5 February 201. Check date values in:

|access-date=(help) - ↑ Fletcher, Nick (9 December 2011). "European leaders resume Brussels summit talks: live coverage". The Guardian. London. Retrieved 9 December 2011.

- ↑ Faiola, Anthony; Birnbaum, Michael (9 December 2011). "23 European Union leaders agree to fiscal curbs, but Britain blocks broad deal". Washington Post. Retrieved 9 December 2011.

- ↑ Chris Morris (2011-12-09). "UK alone as EU agrees fiscal deal". Bbc.co.uk. Retrieved 2012-05-16.

- ↑ End of the veto honeymoon? Cameron on backfoot over euro policy Politics.co.uk, Ian Dunt, Friday, 6 January 2012

- ↑ John Rentoul, "any PM would have done as Cameron did" The Independent 11 Dec 2011

External links

- The EU Crisis Pocket Guide by the Transnational Institute in English (2012) - Italian (2012) - Spanish (2011)

- 2011 Dahrendorf Symposium – Changing the Debate on Europe – Moving Beyond Conventional Wisdoms

- 2011 Dahrendorf Symposium Blog

- Eurostat – Statistics Explained: Structure of government debt (October 2011 data)

- Interactive Map of the Debt Crisis Economist Magazine, 9 February 2011

- European Debt Crisis New York Times topic page updated daily.

- Tracking Europe's Debt Crisis New York Times topic page, with latest headline by country (France, Germany, Greece, Italy, Portugal, Spain).

- Map of European Debts New York Times 20 December 2010

- Budget deficit from 2007 to 2015 Economist Intelligence Unit 30 March 2011

- Protests in Greece in Response to Severe Austerity Measures in EU, IMF Bailout – video report by Democracy Now!

- Diagram of Interlocking Debt Positions of European Countries New York Times 1 May 2010

- Argentina: Life After Default Sand and Colours 2 August 2010

- Google – public data: Government Debt in Europe

- Stefan Collignon: Democratic requirements for a European Economic Government Friedrich-Ebert-Stiftung, December 2010 (PDF 625 KB)

- Nick Malkoutzis: Greece – A Year in Crisis Friedrich-Ebert-Stiftung, Juni 2011

- Rainer Lenz: Crisis in the Eurozone Friedrich-Ebert-Stiftung, Juni 2011

- Wolf, Martin, "Creditors can huff but they need debtors", Financial Times, 1 November 2011 7:28 pm.

- More Pain, No Gain for Greece: Is the Euro Worth the Costs of Pro-Cyclical Fiscal Policy and Internal Devaluation? Center for Economic and Policy Research, February 2012

- "Liquidity only buys time" – Where are European experts for a long-term and holistic approach? Interview with Liu Olin: The Euro Crisis. A Chinese Economist's View. (03/2012)

- Michael Lewis-How the Financial Crisis Created a New Third World-October 2011 NPR, October 2011

- This American Life - Continental Breakup NPR, January 2012

- Global Financial Stability Report International Monetary Fund, April 2012

- OECD Economic Outlook-May 2012

- "Leaving the Euro: A Practical Guide" by Roger Bootle, winner of the 2012 Wolfson Economics Prize

- "Breaking the Deadlock: A Path Out of the Crisis"

- The Eurozone Crisis - Can Austerity Foster Growth? The World Bank's Chief Economist EMEA, Indermit Gil, about potential ramifications, CFO Insight Magazine, July 2012

Euro topics | |||||||

|---|---|---|---|---|---|---|---|

| General | |||||||

| Administration | |||||||

| Fiscal provisions | |||||||

| History | |||||||

| Economy | |||||||

| International status | |||||||

| Denominations | |||||||

| Coins by issuing country |

| ||||||

Potential adoption by other countries |

| ||||||

| Currencies yielded |

| ||||||

| |||||||

| |||||||