Inheritance Tax (United Kingdom)

| Taxation in the United Kingdom |

|---|

|

| UK Government Departments |

| UK Government |

| Scottish Government |

| Welsh Government |

|

| Local Government |

|

In the United Kingdom, Inheritance Tax is a transfer tax. It was introduced with effect from 18 March 1986 replacing Capital Transfer Tax. The current rate charged is 40% of the value of estates over £325,000, or 36% if at least 10% of the estate is given to charity.[1]

History

Prior to the introduction of a single Estate Duty by the Finance Act 1894, there was a system of five different inheritance taxes, that applied to either realty (land) or personalty (other personal property).

- From 1694, Probate Duty, introduced as a stamp duty on wills entered in probate in 1694, applying to personalty.

- From 1780, Legacy Duty, an inheritance duty paid by the receiver of personalty, graduated according to consanguinity

- From 1853, Succession Duty, a duty introduced by the Succession Duty Act 1853 applying to realty settlements taking effect on the death of the settlor

- From 1881, Account Duty applied as an anti-avoidance duty on lifetime gifts made to avoid paying Legacy Duty

- From 1889, Temporary Estate Duty, an inheritance duty paid by the receiver, applying to both realty and personalty, graduated according to consanguinity

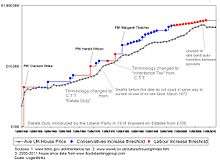

Following the introduction of a single Estate Duty in 1894 the rates were increased which led in many cases for the first time to the breaking up of large estates. Estate Duty began, at a more typical rate of tax, starting in 1914 under the First Asquith ministry[2] that was a breakthrough in constitutional terms and social terms by introducing the People's Budget and the first written right of the House of Commons to ascendancy in the Parliament of the United Kingdom under the Parliament Act 1911.

In 2007, 94% of all estates escaped Inheritance Tax, mainly because they fell in the nil rate band.[3]

Estate Duty was replaced in 1975 by Capital Transfer Tax, which was renamed Inheritance Tax (IHT) in 1986. There are a few simple and widely used methods available to avoid it, often resulting in additional income and capital gains taxes on trusts; however, Inheritance Tax accounts for about 0.8% of government income, raising around £2 billion in 2001[4] and around £2.7 billion in 2011.[5]

Nil rate band thresholds – transferable to surviving spouse(s)

A spouse exemption has long existed in respect of Inheritance Tax as a matter of public policy. From 9 October 2007, a transferable nil rate band policy was introduced that allows a surviving spouse (who has lost a husband/wife/civil partner) to benefit from an additional percentage of nil rate band (that unused) therefore providing up to a 200% nil rate band for that person; however that person may have already used their nil rate band, for instance to provide for relatives less likely to face care charges under the (National Health Service and) Community Care Act 1990. For the 2010/2011 tax year, the IHT rate was 0% on the first £325,000 (the "nil-rate band"), and 40% on the rest of the value, at death, of an individual's taxable estate (loosely speaking net assets at death as the tax provides for a degree of retro-activity as at date of death).[6]

The tax is payable on only the value of an estate above the nil rate band.

In the 2007 budget report the Chancellor of the Exchequer announced that the nil rate band was to rise to £350,000 by 2010. This plan was said to take into account the sharp rise in house prices in the United Kingdom over the previous few years.[7] This increase was cancelled by the Chancellor in December 2009 and while in the 2008–2012 global recession has been maintained at £325,000 until at least the end of the tax year ending 5 April 2016.[2]

It is worth noting that as the Government seeks not to profit from the death of those who a) gave their lives in military service, or b) died from the results of a wound, injury, or disease associated with that military service, that the estates of such servicemen and women are exempt, totally, from any Inheritance Tax regardless of the value of the estate even if it amounts to millions of pounds as long as a) or b) apply....and that that exemption is then transferable to the serviceman's or servicewoman's widow or widower. That they do qualify as at a) or b) may be certified by application to the British MOD "Joint Casualty and Compassionate Centre" (JCCC). The JCCC then inform the HMRC of that decision. The exemption does not apply to ex-servicemen or servicewomen who die from other causes unrelated to their military service.

Tax estate

The tax estate includes:

- all of the deceased's assets, whether real estate or personal estate, and includes even small-value items such as the contents of his or her home;

- any gifts not reasonable presents (e.g. see birthday or see marriage below) or gifts of income not affecting the lifestyle or affecting significantly the finances of the person made by the deceased in the seven years before death (subject to a tapered relief for each year within the seven years);

- some assets which were not owned by the deceased but which are affected by the death (the most common example is a life interest in a trust, also technically known as an interest in possession);

- gifts with reservation of benefit. These are gifts where the legal ownership passes to the recipient. However, the donor continues to enjoy the benefit of the asset either rent free or at reduced cost. The seven-year period outlined above does not begin counting down whilst a gift is considered to be under a reservation of benefit.

There is also a charge on "lifetime chargeable transfers" into certain trusts (and a recalculation of those charges if the giver dies within seven years), and trusts themselves have an inheritance tax regime. See Taxation of trusts (United Kingdom).

Deductions

There are deductions for:

- all assets left to a UK-registered charity.

- some political donations to major political parties.

- gifts of up to £3,000 in total in a given year.[8]

- "small gifts" of up to £250 made to separate individuals.

- some business assets (under Business Property Relief or "BPR").

- some farmland (under Agricultural Property Relief or "APR").

- gifts made out of income that do not affect the standard of living of the donor.

- gifts made in contemplation of a marriage or civil partnership. The allowance ranges from £5,000 to £1,000 according to the closeness of the relationship of the donor to the person marrying or entering into a civil partnership. £5,000 for close family, e.g. wife and children, £2,500 for grand children, £1,000 for anybody else.

- quick succession relief (whereby a person inherited an asset and died soon after), relief is given on the asset inherited in order to prevent double taxation.

Minimising IHT

In order to avoid IHT, many people in the IHT bracket practise some or all of the following avoidance measures:

- Outright gifts to another individual made during a person's lifetime are known as "potentially exempt transfers" or PETs. They are taxable if the person dies within seven years but have the potential to become exempt from tax once the donor survives seven years. There is no reduction in inheritance tax if the donor dies within three years of the transfer. However, if the donor survives three years, the rate of tax on the PET reduces by one fifth (to 32%) and then by a further fifth on each of the subsequent anniversaries (to 24%, 16% and then 8%) until the PET is fully exempt from inheritance tax after seven years. This is known as inheritance tax taper relief (not to be confused with the better-known capital gains tax taper relief).

- Giving assets to a trust fund before death. (Some gifts of this kind, however, are disadvantageous as they amount to lifetime chargeable transfers on which half the IHT is due immediately if the cumulative total of chargeable gains gifted exceeds the nil-rate band (£325,000 in 2015/16). This applies to many more trusts, including discretionary/flexible trusts, than previously under legislation introduced by the 2006 budget. Any Tax that is charged on a Trust during the lifetime of the deceased is not recoverable, even if the total estate is below the nil rate band. See Taxation of trusts (United Kingdom).)

- Certain special types of trust, such as a Discounted Gift Trust, which allow for capital to be given whilst retaining a lifelong access to an income stream from said capital (and which, where the settlor is in reasonably good health, are one of very few planning arrangements with an immediate reduction in inheritance tax liability), and gift and loan Trusts.

- Inheritance tax solutions based around Business Property Relief qualifying investments, including Enterprise Investment Schemes.

- Charitable giving, which is IHT exempt.

- Lifetime gifts within certain limits are completely exempt. These include any number of "small gifts" (up to £250 per recipient per year), an annual amount of £3,000, all regular gifts from surplus income, and some wedding gifts.

- Upon death (by will or intestacy) the passing of non-taxable assets to the next generation (or to a discretionary trust for the benefit of the whole family) and therefore not to the spouse. This may seem counterintuitive because both current and future gifts to a spouse are IHT exempt and were therefore before 2007 to be maximised. However, if something is non-taxable on the first death it should not go to the spouse as it will merely increase their tax estate upon their later death. (The nil-band discretionary trust, discussed below, is an example of this principle in action.) Following the October 2007 change, this strategy may no longer be necessary, and may if the nil rate band threshold increases to reflect perhaps expected average rises in wealth result for wealthier couples (i.e. with current combined wealth over £650,000) in less tax-free estate for a couple's beneficiaries.

- Selling one's property to a home reversion plan, which is a type of Equity release scheme and using the resulting income stream to fund a life insurance policy, written in trust for the beneficiaries, so as to replace the lost value of the property.

Nil-rate band

The Chancellor of the Exchequer's Autumn Statement on 9 October 2007 [9] announced that with immediate effect inheritance tax allowances (often referred to as the nil-rate band) were to be transferrable between married couples and between civil partners. Thus, for the 2007/8 tax year, a married couple will in effect have an allowance of £600,000 against inheritance tax, whilst a single person's allowance remains at £300,000. The mechanism for this enhanced allowance is that on the death of the second spouse to die, the nil rate band for the second spouse is increased by the percentage of the nil-rate band which was not used on the death of the first spouse to die.

For example, if in 2007/08 the first married spouse (or civil partner) to die were to leave £120,000 to their children and the rest of their estate to their spouse, there would be no inheritance tax due at that time and £180,000 or 60% of the nil-rate band would be unused. Later, upon the second death the nil-rate band would be 160% of the allowance for a single person, so that if the surviving spouse also died in 2007/08 the first £480,000 (160% of £300,000) of the surviving spouse's estate would be exempt from inheritance tax. If the surviving spouse died in a later year when the nil-rate band had reached £350,000, the first £560,000 (160% of £350,000) of the estate would be tax exempt.

This measure was also extended to existing widows, widowers and bereaved civil partners on 9 October 2007. If their late spouse or partner had not used all of their inheritance tax allowance at the time of the spouse's death, then the unused percentage of that allowance can now be added to the single person's allowance when the surviving spouse or partner dies. This applies irrespective of the date on which the first spouse died, but special rules apply if the surviving spouse remarries.

In a judgement following an unsuccessful appeal to a 2006 decision by the European Court of Human Rights, it was held that the above does not apply to siblings living together. The crucial factor in such cases was determined to be the existence of a public undertaking, carrying with it a body of rights and obligations of a contractual nature, rather than the length or supportive nature of the relationship.[10]

Prior to this legislative change, the most common means of ensuring that both nil-rate bands were used was called a nil band discretionary trust (now more properly known as NRB Relevant Property Trust*). This is an arrangement in both wills which says that whoever is the first to die leaves their nil band to a discretionary trust for the family, and not to the survivor. The survivor can still benefit from those assets if needed, but they are not part of that survivor's estate.

Pre-owned assets

The Finance Act 2004 introduced a retrospective income tax regime known as pre-owned asset tax (POAT) which aims to reduce the use of common methods of IHT avoidance.[11]

Controversy

In 2002, Queen Elizabeth The Queen Mother is understood to have left her entire estate (estimated at £50 million) to her daughter Elizabeth II, including works of art, jewels, antiques and her thoroughbred racehorses. A deal made back in 1993 ensures that The Queen is spared inheritance tax of an estimated £20 million on her mother's estate.[12][13]

In 2016, calls have been made to reform the UK's system of trusts. Pressure groups have called for trusts to publish annual accounts just like private companies and also for a central register of trusts to be administered. This follows the recent death of the Duke of Westminster where his significant estates, that are to be past down to his children, are thought to be largely free from inheritance tax.[14]

Political discussion

Inheritance Tax has been something of a political football with the government of the time introducing the concept of a transferable nil-rate band (NRB) on 9 October 2007 and the opposition promising to significantly increase the NRB threshold to £1 million. However, the Coalition government has agreed to keep the threshold for the time being.

See also

- Asset-based egalitarianism

- Disclaimer of interest (including Deed of Variation)

- History of the English fiscal system

References

- ↑ , Moneysavingexpert.com UK Inheritance Tax

- 1 2 "Rates and allowances: Inheritance Tax thresholds".

- ↑ "BBC NEWS - UK - UK Politics - Axe inheritance tax, Tories urged".

- ↑ accessed 22 May 2007

- ↑ Adam, Stuart and Browne, James (November 2011) A Survey of the UK Tax System The Institute For Fiscal Studies, Briefing Note No. 9, Accessed 5 April 2012

- ↑ "Inheritance Tax planning / Estate planning / Trust returns & wills".

- ↑ "MSN Money UK - Latest business news, money news and advice". money.uk.msn.com. Retrieved 21 March 2007.

- ↑ HMRC - Annual Exemptions

- ↑ 2007 Pre-Budget Report and Comprehensive Spending Review: 01

- ↑ Hilary Osborne. "Sisters lose fight for tax rights of wedded couples". the Guardian.

- ↑ REV BN 40: Tax Treatment Of Pre-Owned Assets

- ↑ "Mr Major's Commons Statement on Royal Taxation - 11th February 1993".

- ↑ "Palace fear over Queen's tax bill". Mail Online.

- ↑ "Inheritance tax: why the new Duke of Westminster will not pay billions". The Guardian.

External links

- Certainty the National Will Register

- Instantly calculate your inheritance tax liability free with the Which? group

- Revenue and Customs Inheritance Tax

- List of UK Regional Probate Registries - Regional Offices for probate information and to register the location of a Will and/or Executor

- Inheritance Tax Explained (VIDEO)

- Free guide to inheritance tax from Hargreaves Lansdown